Africans in the United States must remember that the slave ships brought no West Indians, no Caribbeans, no Jamaicans or Trinidadians or Barbadians to this hemisphere. The slave ships brought only African people and most of us took the semblance of nationality from the places where slave ships dropped us off. – Dr. John H. Clarke

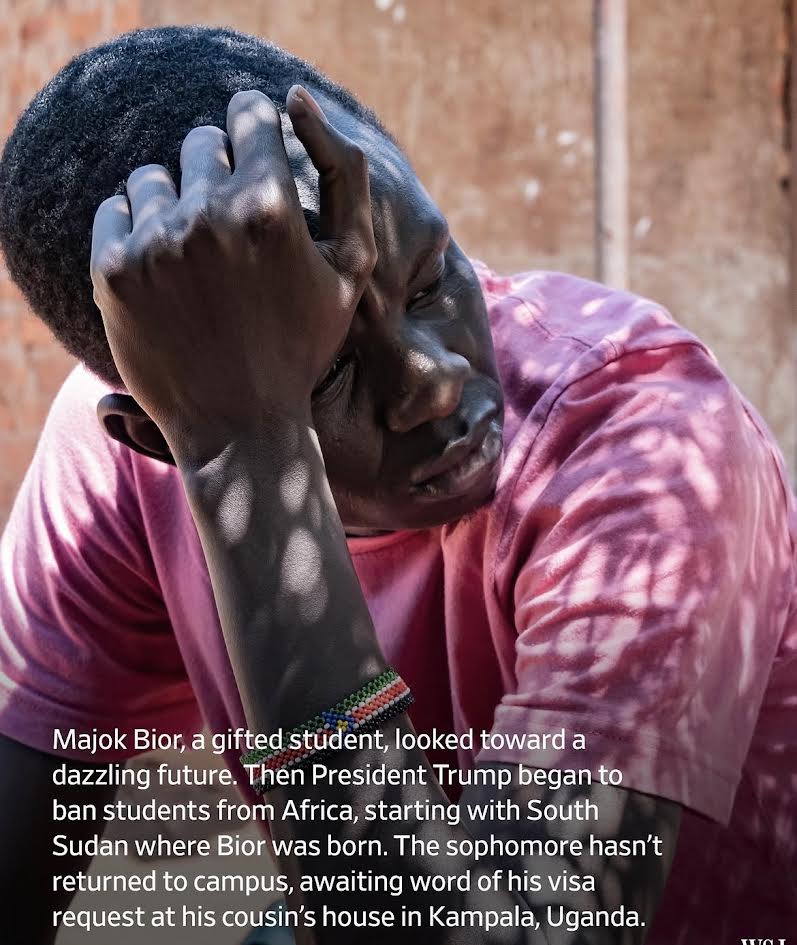

The photograph of Majok Bior, a South Sudanese computer science sophomore at Duke University, stranded at his cousin’s home in Kampala after the Trump administration’s travel restrictions invalidated his visa — has circulated widely as a symbol of individual suffering. And it is that. But to read it only through the lens of personal tragedy is to miss the structural dimensions of what is unfolding across American higher education, and to miss, in particular, what this moment means for HBCUs.

The Trump administration’s travel ban, initially signed on June 4, 2025, targeted 12 countries and placed partial restrictions on seven more, covering a geography concentrated in Africa and the Middle East. By December 2025, that list had expanded to 39 countries and territories, with Nigeria, historically one of the top ten sources of international students in the United States, placed under partial restrictions effective January 1, 2026. Individuals in Nigeria will not be able to receive student visas beginning January 1. Secretary of State Marco Rubio has signaled further expansion, with a State Department memo identifying 36 additional countries for potential restriction, including 25 African nations as well as countries in the Caribbean, Central Asia, and the Pacific Islands. If that expansion proceeds, the policy will have effectively severed the institutional connection between American higher education and the African continent.

For HBCUs specifically, this is not a distant geopolitical event. It is a direct threat to an enrollment strategy, a revenue base, and a civilizational relationship that institutions have spent decades building.

To understand the financial stakes, one must first understand how international student enrollment became integral to the fiscal architecture of many HBCUs. In addition to the tuition money international students often bring, many foreign students pay the full sticker price, often aided by their home countries’ governments there are benefits for HBCUs’ American students as well. International students, particularly those arriving with government-funded scholarships from Nigeria, Ghana, Saudi Arabia, and other nations, have served as a reliable source of full-fare tuition revenue at institutions that chronically lack the endowment depth to absorb enrollment volatility.

Among HBCUs with ten or more international students, Morgan State had the most as of the 2017-18 academic year, with 945 students; Howard was second with 920; and Tennessee State third with 584, according to the Institute of International Education. These numbers have only grown. Tennessee State, for instance, went from 77 international undergraduate students in 2008-09 to 549 by fall 2016 representing roughly 8 percent of its undergraduate student body. Across the sector, African students from Nigeria and Ghana historically constituted a significant share of that international cohort.

The financial logic was sound. A university with modest endowment holdings and only one HBCU, Howard University, currently holds an endowment exceeding $1 billion, cannot easily absorb the loss of a tuition-paying population without triggering cascading institutional consequences. When full-fare international students leave an enrollment ledger, the institution must either raise tuition on domestic students who are often already Pell Grant-eligible, draw down reserves, reduce staffing, or curtail academic programs. In a sector where financial fragility is not the exception but the norm, any of those choices carries compounding institutional risk. Preliminary projections by NAFSA and international education research partner JB International predict a 30 to 40 percent decline in new international student enrollment, leading to a 15 percent decline in overall enrollment this fall and loss of $7 billion within local economies and more than 60,000 jobs. That system-wide figure masks the disproportionate exposure at institutions whose international student populations are concentrated in African countries now under restriction.

The financial dimension, however, is only the first tier of the problem. The more consequential loss may be strategic: the slow dismantling of an institutional relationship between HBCUs and Africa that has been a defining feature of both parties’ long-term development. For decades, HBCU campuses have served as one of the primary entry points for African students seeking American credentials and professional networks. The relationship has never been purely transactional. It has been civilizational, rooted in a shared recognition that the institutional capacity of the African diaspora, on both sides of the Atlantic, depends on the training and circulation of its most capable people. Howard University, Morgan State, Florida A&M, and Tennessee State have all cultivated significant African student communities that returned home as engineers, physicians, lawyers, economists, and public administrators, seeding institutions across the continent with HBCU-educated professionals.

That pipeline is now interrupted. Majok Bior is one face of the disruption. He is also, statistically, the kind of student, a full-scholarship computer science talent, whose skills and networks would have contributed meaningfully to either the American or the African institutional ecosystem over the subsequent decades. The State Department’s position is unambiguous. There is no appeals window, no informal pathway, no consular discretion available to students like Bior whose visas were invalidated mid-enrollment. The pipeline does not merely slow. It stops.

The administration has signaled it may further target sub-Saharan Africa for future travel bans. Twenty-four of the 36 countries identified as future ban candidates are in sub-Saharan Africa. If all 24 were to be hit with bans, an additional 71 percent of the region’s population would be affected. At that scale, the policy would not merely interrupt an enrollment channel. It would functionally close the institutional bridge between American HBCUs and the African continent.

The arrivals data make the stakes concrete. The number of new and returning African students arriving in the United States for the 2025 fall semester fell by nearly a third from the previous year, according to preliminary Commerce Department data. Arrivals from Nigeria and Ghana, which historically send more students to the United States than any other African countries, dropped by roughly half. Those are not marginal declines. They represent a structural break in the flow of talent that has sustained both HBCU campuses and the professional networks those campuses anchor.

The broader context amplifies the damage. HBCUs have been managing a long-running tension between their mission to serve African American students and the enrollment arithmetic that increasingly pushes them toward diversification. Black student enrollment at HBCUs increased by just 15 percent from 1976 to 2022, while enrollment of students from other racial and ethnic groups rose by a staggering 117 percent during the same period. Within that context, African international students have occupied an important, if underappreciated, position: they are enrolled students who are Black, who arrive often with external funding, and who align with the cultural mission of the institution in ways that students from other international communities do not. The loss of this population does not merely reduce headcount. It removes a category of student whose presence reinforces the intellectual and cultural identity of HBCU campuses while simultaneously contributing to their revenue base.

HBCU leaders should resist the temptation to treat the current moment as a policy problem requiring a policy solution that is, to wait for a change in administration or a favorable court ruling before taking action. The institutional response must be proactive, and it must be organized at the sector level rather than institution by institution.

The first imperative is legal and advocacy coordination. HBCUs should be visible participants in the coalition of higher education institutions pushing back against travel ban expansion. The legal challenges already filed by some universities have produced limited court-ordered exceptions. HBCU presidents, through their associations and individually, possess a particular moral authority in this argument: these institutions were founded on the principle that the state should not determine who deserves access to education. That founding logic has direct application to the current moment, and its articulation should not be left to the advocacy organizations of predominantly white institutions alone.

The second is the construction of alternative enrollment infrastructure. Several countries whose students are not currently restricted represent significant untapped pipelines for HBCUs including Kenya, Ethiopia, South Africa, and several francophone West African nations not yet under full restriction. Morgan State’s international enrollment tripling between 2014 and 2017, driven by a concerted recruitment strategy, demonstrates that rapid scaling is possible when institutions make it a priority. The question now is whether that kind of deliberate enrollment strategy can be retargeted toward countries where the policy environment remains navigable.

The third imperative, and the most consequential for the long run, is the development of transnational academic infrastructure that does not depend on American visa policy at all and here the sector does not need to theorize. It already has a model. Claflin University, an HBCU in Orangeburg, South Carolina, and Africa University in Zimbabwe have together built and delivered a fully online Master of Science program in Biotechnology and Climate Change, producing their first cohort of graduates in 2025. The program requires no visa, no transatlantic relocation, and no dependence on the goodwill of a State Department consular officer. It delivers graduate-level credentials, anchored to an HBCU’s academic infrastructure, to scholars who remain embedded in the African communities they will eventually serve. That is not a symbolic gesture. It is a replicable institutional architecture — one that severs the link between American immigration policy and the HBCU-Africa educational relationship at precisely the point where that link has proven most vulnerable. The disciplines selected are themselves strategic: biotechnology and climate change are among the fields where African scholars have the most urgent applied work to do, and where the absence of well-trained researchers carries the steepest institutional cost. What Claflin and Africa University have built is a proof of concept for the entire sector. Howard, Morgan State, Florida A&M, and Tennessee State, institutions that have already invested in African student pipelines and cultivated international enrollment are positioned to extend this model into additional disciplines, additional partner institutions, and additional countries. Students who were considering coming in 2026 will be discouraged and will be looking to other destinations, as one international education expert has observed. If those students go elsewhere, HBCUs should be competing to ensure that some of that “elsewhere” is a degree program bearing an HBCU’s name, delivered on African soil, through African partner institutions, and impervious to the policy preferences of any particular American administration.

The image of Majok Bior waiting in Kampala is a human document. But it is also an institutional document. It records the moment when an African student who had successfully navigated the American credentialing system, who had won a full scholarship, enrolled in computer science, played intramural soccer, and survived chemistry class was extracted from that system not by any failure of his own but by a federal policy aimed at restricting the movement of African people into American institutions. HBCUs were built precisely because such exclusions were once the default condition of American higher education. The institutional memory of that history is not a rhetorical resource. It is a strategic asset, a basis for understanding that the institutions which serve communities without consistent access to political protection must always be building structures that can survive the withdrawal of that protection. The Africa travel ban is an HBCU problem. The sector’s response to it will reveal something important about whether these institutions have developed the depth and coordination to meet a challenge that is, in its essential structure, the same challenge they were built to confront.

Disclaimer: This article was assisted by ClaudeAI.